How to Grow Cup & Saucer Vines

November 28, 2019

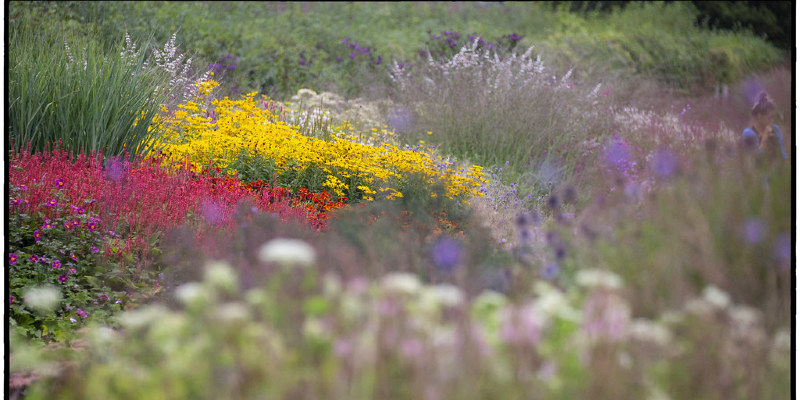

Cobaea scandens, better known by the frequent name cup-and-saucer vine or cathedral bells, is a fast-growing plant that is hardy in U.S. Department of Agriculture planting zones 9 through 11. In warmer climates such as California, gardeners can enjoy it; although in most of the nation, this plant has been grown as an annual. Using its own cup – or bell-shaped green-to-purple or white blooms, the plant blooms when planted from seed, and sets up a thick screen of evergreen foliage, developing 25 feet in 1 season. Gardeners in regions have a bit of gratification, together with the flowers that are gaudy not making an appearance.

Starting from Seed

Nursery-grown cup-and-saucer vine seedlings are tough to locate, therefore starting from seed is your best option. Easily available online and on seed racks that are high heeled , they are slow to get going and tricky to germinate, so begin indoors six to eight weeks prior to the temperature warms up. Fill peat pots with mix — prepare baskets than the number with, since the seeds are difficult to germinate. Moisten the potting soil and nick the seed coat together its border that is longer . Press on the seed, then nicked border down, into the potting soil, therefore it’s just barely covered with soil. The seeds should germinate in 10 to 24 days, if kept moist and in a room where the temperature is Fahrenheit.

Site Considerations

Clear incorporate compost into a website from the garden near fence or a sturdy arbor that is in full sun and weeds. The website should also have well-draining soil. If you are uncertain how to tell when you’ve got well-draining soil, dig a 1-foot hole in which you wish to plant and then fill it with water. Let it drain and refill the hole. Stick at a yardstick and take a measurement of the water. Wait an hour and place the yardstick in again. If the water has gone down less than 2 inches, then the soil isn’t draining well, pick on another website. Vine requires some protection therefore it won’t be a fantastic fit for a number of gardens.

Planting

Once nighttime temperatures are consistently about 50 degrees F plant your cup-and-saucer vine seedlings outside. About a week before you expect to plant them, set your seedlings outside in a protected area — first for an hour or twolonger daily till they are out. Tear off any rim of the peat pot that extends above the soil level in the pot and then pop up the seedling — bud and all — in your website. Place them 24 to 36 inches apart if you are planting over one Cobaea scandens. Water well. Top of organic mulch.

Culture

Keep the plant moist although it’s established, but allow the 2 inches of soil to dry between waterings — test with your finger to be sure. It’s fairly drought tolerant once the plant has been established. Wilting leaves will tell you it requires more water. Fertilizer generally isn’t necessary the first year; but in future years, feed it. Avoid high-nitrogen fertilizers to promote flowering.

Maintenance

Since the plant grows, it produces tendrils from the ends of the terminal leaves on each stem cells, which wrap around surfaces such as cable, fence links or lattice to climb without help. You may need to initially guide the leader onto the support by tying it loosely to the aid with twine. Pinch off or redirect infantry branches if you want this wild grower to go in a specific 21, as they grow. Pinching the end of a pruning and stem branches off off low helps promote foliage at the base of the plant — helpful if you are using your cup-and-saucer vine. Seed pods shape from the fall, and you may have volunteer seedlings that you will need to remove. Clean up lost seed pods as well as dropped leaves in the fall. Trim back some of the oldest stems from the spring to promote new growth if the vine yearlong’re growing of the plant. Renew mulch every year.

How to Propagate Cold Hardy Bamboo

November 23, 2019

Bamboo is for the tropics. When you pick the selection, it offer a little privacy or can be a exotic point. Bamboo can be”running” or”clumping.” Runners would be the invasive creatures that provide a name, when planted with no root barrier, taking over landscapes to the large-scale grass. Bamboo stays put, just expanding several inches a year, though it can look equally as dramatic. Bamboo, which has the name Fargesia that is genus, is a clumping, evergreen bamboo. Whenever you have a cold-hardy, clumping bamboo plant that you want more of — or want to share — propagate it.

Inspect the pine plant — at least 2 full years old — you intend to split in the spring to make sure new shoots have not started to push up through the floor. Before shoots arise to your best shot at success, bamboo has to be split. Pay special attention to regions where you will find one or two canes, also called culms . These are the simplest to separate from the plant and last season’s new growth.

Cut off the of this culm you are going to split with loppers or a handsaw and remove most of the small stems of foliage below the cut. This also helps the bamboo branch recover since it can concentrate energy on roots and loses less water. You are able to leave the ones undamaged, which means that your branches won’t look quite so gloomy and barren, if there are canes.

Water the plant and the floor around it. Wait 24 hours.

Position a shovel between the mother clump and the regions of new growth’s line you are going to split. Drive down firmly — this generally means your feet will need to get into the action as well, standing on the flanges on top of the shovel head to use your body to cut although the fibrous rhizome that joins the area of new expansion to the mother plant.

Move with the shovel around the area of new growth, leaving a margin of 6 to 8 inches around the clump until you can pop the piece you have dug.

Put the root ball in a plastic garbage bag and set it in the shade to help it retain moisture for those who have more branches to dig; otherwise, move to Step 7.

Dig a hole twice as wide as the root ball and as heavy in a place of your lawn with well-drained dirt and full to partial sun — meaning it doesn’t stay waterlogged after a rain.

Loosen the soil and around its edges with the blade of the shovel and mix in a few all bone meal, blood meal and cotton seed meal.

Place in the middle of this hole and then refill it with the dirt your removed, firming it around the bamboo plant that is new. You may stake the plant — with bamboo sticks, naturally — to keep it from being dismissed until its roots start to establish. Just push on a pole and then attach it loosely to the stake with plant ties.

Water before the soil is wet to a depth of 12 inches — check the time to gauge just how much water it takes. Allow the top 3 to 4 inches of soil dry out between waterings, but maintain the transplant moist, so monitoring it for the first few months. When the leaves start to curl in on themselves, more water is needed by the plant.

Mulch in the autumn with leaves from the mommy bamboo plant. Composted horse manure or A high-nitrogen fertilizer could be applied.

How to Install a Shower Rod in Marble

November 20, 2019

Exactly the hard surface that gives its traditional beauty to marble makes it an unforgiving substance with which to work. When installing a shower pole in a marble bath This creates a dilemma. Sticks work but lack a sound look. It needs one to drill holes, although A pole mounted with mounts provides that solidity. The task sounds harder than it is, as long as you take your time and use the right tools and technique.

Determine the space from the rear wall of the enclosure to allow the shower curtain to hang in the position, in addition to the height where you want to mount the shower pole. Place a bit of duct tape on the wall at this spot on both sides of the shower enclosure. Measure carefully and draw a large”X” on the two bits of tape, with the center of the”X” marking where you want the center of the shower pole bracket to be.

Build brackets and the shower rod. While you hold another, have a helper hold one end of the pole in position. Place a level on top of the pole. If the pole is not level, raise one side or another slightly until it’s, keeping the bracket consistent with the”X” on the tape as you do this. As a way to create a mark on the tape for every screw 21, use the holes.

Select sized to the plug-type wall anchors as recommended by the pole manufacturer for use or as well as the shower pole. Mount the piece into the chuck of a power drill. Drill a hole in the masonry at each of the marked places. Without trying to force the piece through the substance at drill speeds that are lower and work. Lubricate the piece with clean water since you drill the holes. Stop drilling whenever the marble has been pierced through by you and carefully withdraw the piece.

Gently tap on a wall anchor into each of the holes with a hammer. Have a helper hold the shower pole as it is mounted by you at each end using the screws supplied with the wall anchors.

The Way to Insulate Existing Floors

November 16, 2019

Unwanted air to get into your home is allowed by an uninsulated floor. This cold atmosphere brings down the temperature of your home, leading to wasted energy and higher heating costs during the winter. Improve the energy efficiency score of your home with the addition of insulation to your floor. Oftentimes, you can bring insulation up to recommended levels in just a couple hours without the hassle and cost of removing your existing floor finishes.

Insulate an Existing Wood-framed Floor

Put on a dust mask and safety goggles to protect yourself when managing insulation.

Find the trap door or access panel which allows you to enter the crawl space below your home, or simply put in your basement if you have one. Inspect your floor framing and assess the depth of the existing insulation, if any.

Multiply the total inches of insulation by 3.2 to gauge the present R-value of your floor. If you have two inches of insulation, your floor has an R-value of 6.4. Most homes need at least R-13, though houses in cold areas can benefit from more insulation.

Calculate how much insulation to include. Assuming you currently have two inches of fiberglass, you’ll want to include at least two more inches to achieve R-13. If you would like to accomplish a greater R-value, gauge how many inches you want to grow achieve that number if each inch adds R-3.2 to the ground.

Cut your insulation to size using a utility knife. Put it in the space between your existing floor joists, relying on friction to hold it in position. Insert wire insulation hangers as needed to ensure a secure hold.

Insulate Existing Concrete Floors

Cover the whole floor using a vapor barrier, for example 6 millimeter polyethylene sheeting. Overlap the seams of this vapor barrier by 6 inches and fasten the seams with tape. Secure the edges of the plastic to the slab using structure caulk.

Measure 16 inches from the surface of a single wall. Mark this dimension on the ground with chalk, then continue to make marks every 16 inches throughout the period of the ground.

Put a length of 2-by-2-inch lumber on every one of the marks you made to make timber sleepers, or furring strips. Use concrete screws to maintain the sleepers in place.

Cut rigid foam insulation to fit snugly between each table. Score and snap the foam by means of a utility knife. Insert two layers of rigid foam to achieve the highest potential R-value at the tiniest amount of space.

Cover the whole surface with sheets of 3/4-inch plywood, then lining up the edges of each sheet onto the center of their sleepers. Stagger the joints between rows of plywood to improve floor stability. Nails the plywood to the sleepers using 6d nails every 12 inches.

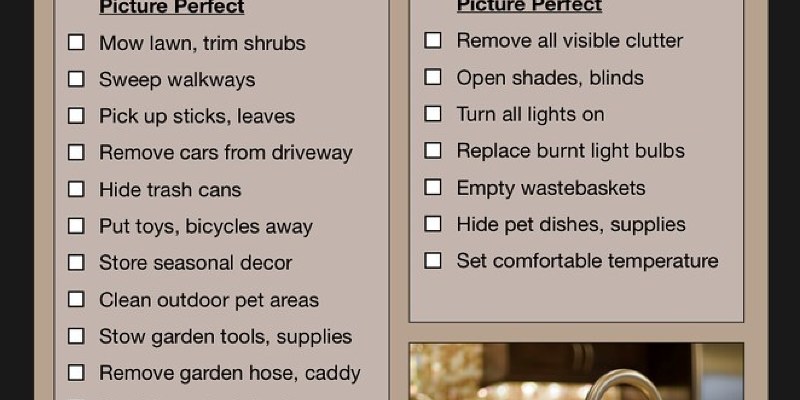

What's a 2-10 Home Buyers Warranty?

November 12, 2019

When cash is tight, an unexpected home repair or the replacement of a system or appliance can cause a severe fiscal crisis. This situation is a possibility. Home warranties such as the 2-10 Home Buyers Warranty can minimize the effect of expensive repairs in both newly built and resold houses.

Identification

The 2-10 Home Buyers Warranty is a name new house warranty. It is available for both new houses and for resale houses. Both warranty types cover big systems, such as heating, air, plumbing and electrical, along with major appliances that came with the purchase of the house, like dishwashers, hot water heaters, stoves, ovens and garage door openers.

Effects

A resale warranty is bought by the vendor before the closing date of the house sale. It covers appliances and systems for an agreed-upon period. Many vendors use this as a marketing tool to create their house more attractive by creating a sense of security for buyers. There are no costly surprises for the buyer, because he won’t need to manage any immediate significant repair expenses. With resale warranties, provided that the damaged part is functioning as soon as the seller buys the warranty, the repair is covered.

Types

A new home warranty is bought by the builder and offered along with any limited builder’s warranty. This helps to verify a buyer’s confidence in the character of the builder’s work. The company’s new home warranty provides two levels of coverage: the”two” represents two years’ coverage for important systems, along with the”10″ represents 10 years’ coverage for all structural defects. On its site, 2-10 Home Buyers Warranty defines this as”real physical harm to one or more of the designated load bearing elements caused by failure of such load bearing elements, which makes it unsafe, unsanitary or otherwise unlivable.” This may incorporate base damage, roof joist failure, buckling of outside walls and frame damage. The limited builder’s warranty typically covers less severe and cosmetic issues for one year. This type of warranty protects buyers while providing builders a way to maintain warranty outlays minimal.

Factors

The warranty is often included among the seller-paid prices at closing, although some sellers buy the warranty the moment they record the house so that warranty protection is in place during the listing period. Not every program is covered and the range of coverage varies; study to whether the warranty provides the ideal level of coverage for the house is important. A home warranty doesn’t take the place of homeowner’s insurance.

Method

When a covered problem happens, the homeowner requires that the warranty firm right and files a claim. The company contracts with experienced regional service providers to perform the necessary repairs. The warranty company touch base with its designated contractor, who then contacts the homeowner to set up a time for the repairs. The homeowner is responsible for a small charge, meant to dissuade people from creating unnecessary claims. The contractor gets the repairs, along with the warranty company pays the contractor directly. If the contractor determines the challenge is irreparable, the corporation will authorize replacement of this merchandise.

Can a Property Owner Evict Tenants Without Reason?

November 9, 2019

Eviction is a stressful ordeal. If you can’t afford to move someplace else, you may be reduced to placing your belongings in storage and subletting a room, living out of a resort or even worse. Eviction means you’ll have a more difficult time. You will be seen by potential landlords . The very best approach to deal with an eviction is not to have one in the first place, and this usually means that you should learn about the reasons where your landlord can evict you.

Eviction Without Reason

There are quite a few reasons that are good which you could be evicted. Your landlord can offer you the boot if you violate the terms of your tenancy, violate the law, do not pay your lease or harass other tenants. But additionally, there are scenarios where your landlord can evict you for no reason. This power is limited depending on the particulars of your lease arrangement, the town where you reside, the type of home you are leasing and the inherent reason the landlord is evicting you for”no reason.”

Discriminatory and Retaliatory Eviction

State legislation protects you from being evicted for discriminatory reasons like your sex or skin color. The legislation also protects you from being evicted for retaliatory reasons, such as having complained to the landlord about some thing that needed repairing, or fixing it yourself and deducting the cost from the next lease payment, or initiating legal action against your landlord because of the condition of your rental unit. More generally, you can’t be evicted for exercising any legal right which inconveniences the landlord.

Location

Some jurisdictions in California have landlord-tenant rules which go above and beyond the nation’s laws. As stated by the California Department of Consumer Affairs,”Some rent control cities require’just cause’ for eviction.” The specifics depend on where you reside, so that your first step must be to look over your city’s website. Additionally, some specific properties operate under special rules that restrict the landlord’s ability to evict you. Generally, your landlord has the best power to evict you arbitrarily when you are renting from a private owner in a market rate. Low-income public home usually offers extra protections to tenants.

Month-to-Month Tenancy Termination

If you are on a month-to-month lease agreement, the landlord has broad discretion to terminate your property without reason, unless it’s criminal to do so. Month-to-month rental agreements do not provide you the very same rights and obligations as a lease, and your landlord can terminate the agreement as readily as possible. This is not an eviction. Your landlord must supply you a 30- or – 60-day notice of conclusion, and also your rental record won’t have any black marks on it. The eviction process may move only in the event that you continue to occupy the house following the 30 or even 60 days have passed.

Lease Agreement Breach

If you are on a rental lease and you breach the terms of the lease, you’ll be evicted. Otherwise, you can’t be evicted for any reason before the lease expires. Read a lease thoroughly before you register this, and request modifications to the language where you think the terms are foolish.

Eviction Versus Termination

“Eviction” is the process of physically barring you from continuing your tenancy, and it can be done only by a sheriff with the proper consent of a courtroom. Your landlord can’t personally evict you under any conditions. The eviction process starts with your landlord serving you a eviction notice, then taking you to court. It’s crucial that you take part in this process in order to protect your rights, and also to employ a lawyer if at all possible. “Termination” refers to the end of the leasing relationship between you and your spouse. This is a necessary precursor to any eviction proceedings against you, and you might not be evicted while your property is still in good standing.

Pros & Cons of Joint Tenants With Rights of Survivorship

November 6, 2019

The way buyers choose title to real estate could be critical, but choices can be confusing and occasionally misunderstood. California enables people to take title as tenants in common, or as joint tenants with right of survivorship. Married couples have the extra option of accepting title as community property. Every one these methods differ slightly to inheritance, ownership and taxation implications.

Ownership Share

A married couple, unmarried couple or unrelated people are able to hold title as joint tenants with rights of survivorship. Joint tenants have to be equal shareholders in the property and all take ownership. Unlike holding title as tenants in common, one individual can’t own a larger proportion of the property than another. Advantages of holding title as joint tenants include each individual having unfettered rights to use, take loans out against or sell the property–in combination with another tenant. Disadvantages might include being unable to partition a property in unequal parts for what ever reason deemed necessary.

Inheritance

1 advantage of taking title as joint tenants with rights of survivorship is a tenant avoids probate when one spouse dies. Probate court proceedings can take weeks and cost thousands of dollars, depending on the complexity of the estate. A joint tenant will inherit the decedent’s portion of the property irrespective of what might be written in a will. The advantage of taking title as joint tenants is the surety that the survivor receives the property quickly, with very little expense and with no complications from conflicting wills or other documents. Individuals who want to leave a part of a property to a family member will have issues accomplishing the task with joint tenancy.

Other Factors

Spouses who fear potential suits targeting the real estate of a recently deceased spouse are protected if they inherit via a joint tenancy with right of success. 1 drawback of joint tenancy is the surviving spouse only receives a stepped-up basis for the half portion of the property the decedent possessed. A stepped-up basis resets the base value of a home bought years prior, to the market value at the date of inheritance. When a surviving spouse goes to sell, she can simply use the stepped-up basis for 50% of the sale. She might end up owing more in earnings in the event the home appreciated a sizable amount through the years.

How Do I Reduce the Premium on My Homeowner's Insurance Policy?

November 4, 2019

Even smart shoppers can have a couple issues working against them in their quest to reduce an insurance policy premium. The age of the house, construction materials used and place can factor into an insurance policy premium. Homes situated outside city limits, positioned further than 1,000 feet from a fire hydrant or in a distance of over seven miles from a fire station will frequently pile additional fees onto an insurance policy premium. Older homes with outdated wiring, a deteriorating roof or chipping paint can affect eligibility for a homeowner’s insurance policy.

Compare homeowner’s insurance policies carrying exactly the very same limitations with seven to 10 different carriers prior to purchasing a policy. Check on the internet with the state department of insurance to receive an overview of carrier prices and company financial ratings in your own state.

Houses with fire extinguishers, smoke detectors and deadbolt locks. Some companies offer additional discounts for having all three of these safety items set up.

Check with a local home-safety expert to inquire about installing a monitored fire or burglar alarm to the premises. Most insurance companies offer discounts of 5 percent to 15 per cent for monitored alarms that alert the police and fire departments to a crisis. Speedy response times might help mitigate damage to a house and dissuade theft.

Bundle a house, cars, business or umbrella policy with the same company. Obtain discounts of 15 percent to 25 percent each automobile when bundling autos with a home, along with 10 percent to 20 percent on a homeowner’s premium. Additional discounts may apply to additional bundled policies.

Keep a clean claims history on a house. Avoid making little claims on homeowner’s policies which can add penalty fees onto the premium and earn a policyholder uninsurable when desiring to switch carriers. Insurance companies frequently have strict underwriting guidelines which analyze past claims when determining whether the new policyholder is an acceptable risk.

Choose a higher house deductible, such as $1,000, which reduces annual premiums and will help homeowners avoid the desire to make a run of small claims.

Keep credit ratings squeaky clean to reap additional savings on a house policy. Policyholders with good credit standing are considered better risks than those with bad credit ratings and can receive additional discounts on a policy.

What Happens If You Get a Foreclosure Notice?

October 30, 2019

In the event you receive a foreclosure notice in the email, it means you have fallen far enough behind on your mortgage payments your lender intends to take your house and sell it off unless you make up payments. Your lender can begin foreclosure if you miss one payment, but many creditors will send an overdue note initially and a note of foreclosure just when you default on several obligations.

A Last Chance

When a creditor sends a mortgage letter, the correspondence usually announces that foreclosure will start within 10 days, according to the Nolo legal site. If you discover a way to pay your creditor the late payments before afterward, and interest and any costs your account has incurred, which will usually block the process going any further.

The Lawsuit

If you can’t bring your payments current, the lender will go ahead and file the litigation. The lender’s attorneys then send you a summons and a formal legal complaint and provide you the time to respond, typically between 15 and 30 days. If you intend to resist the foreclosure in court, then you have to respond, or the court will produce a default decision, probably in the lender’s favor. Responding gives you the right to create a presentation to the judge on the reason you need to keep your property.

Another Letter

If the judge rules in favor of your own lender, the following step is going to be a letter notifying you of the date of purchase. In many states, you may still block the sale if it’s possible to collect enough money to repay the mortgage in full, and foreclosure expenses and other costs.

The Sale

In the event you don’t repay your debts, then the lender will place the house up for auction to the highest bidder. If it does not sell, then your creditor becomes the new owner, Nolo says. Up till that moment, you’re still the owner. It is going to usually take at least 3 months after notification before the house is sold, more if you fought the foreclosure actions.

Eviction

If the house is your private house, you may keep on residing there till you receive an eviction notice, even after the purchase. If the new owner does not ask for lease, you don’t have to pay to stay there. Once you have the notice, events will follow according to the eviction laws of your state.

Nonjudicial Foreclosure

In many states, such as California, lenders use deeds of trust, rather than a mortgage, to secure their claim on the house. If your creditor has a deed of trust, it doesn’t have to go to court to foreclose, and the entire process takes much less time.

How Can a Short Sale Affect FICO?

October 27, 2019

A short sale of a house occurs when a homeowner successfully sells his house for less than is owed on it. Typically, the mortgage creditor forgives the difference between the selling price and the mortgage balance. However, a short sale has the potential to negatively alter the seller's credit background for a time. The seriousness of the effect will be contingent on other variables within the seller's credit record, however.

Short Sales

Most frequently, sellers end up in a short sale situation when they#039;re not able to make mortgage payments. Compounding that misfortune is the simple fact that their homes will also be worth less than what they owe. Homeowners confronting these twin circumstances just have a limited amount of choices available to them. Loan modification is one; foreclosure and repossession by the lending company is another. The final is short-selling the house with the lender's consent.

Credit History

All three scenarios –loan modification, foreclosure, short sale–can affect a homeowner's credit rating. The Fair Isaac Corporation is the credit agency most frequently relied on for this score. It's arrived at by blending a individual 's credit entries with his background of payments. In FICO's eyes, events at a individual 's credit life, like a short sale, may show an inability to meet credit obligations. FICO then adjusts that individual 's FICO score so.

Credit Score Factors

FICO has just improved its veil of secrecy somewhat on how it computes credit scores. If it comes to foreclosures and short sales, it looks like both have the same negative effect on scoring computations. Presently, FICO claims that it deducts 85 to 160 points from a person's entire credit rating. Remember, other negative events, such as overdue mortgage payments, may also have lowered that score before any short sale.

Factors

FICO looks at each short sale. The reason the company does this is because every individual 's credit history is person. Variables used in scoring are voluminous, but certain generalities can be made. One is that a person having a high FICO score stands to lose more than one having a middling or very low score. Consequently, somebody having a rating of 750, for example, could shed more than somebody with a 550.

Outcomes

No matter which way you slice it, a short sale is going to hurt. For you, one 'll have dropped your home. For another, your FICO score and credit rating will be broken. Also, you'll pay more in increased interest, for a time, to purchase most anything on the planet. And it could be up to three years before you're in a position to qualify for a new mortgage. A short sale may even carry negative tax implications.